The countdown is underway for the U.S. Securities and Exchange Commission to decide on the first spot Bitcoin ETF in the United States.

Cryptocurrency Financial News

The countdown is underway for the U.S. Securities and Exchange Commission to decide on the first spot Bitcoin ETF in the United States.

The unsecured bond has a value of 10 million euros and a maturity of three years, with all the proceeds going for eligible green activities investments.

The Bureau of the Treasury has set a minimum target of 10 billion pesos.

Real-world asset tokenization as a concept has existed for some time. However, in 2023, with the growing interest of institutions, various governments have started experimenting with the idea.

The stars are lining up for Bitcoin price, but a few major price threats remain in play.

Paolo Ardoino, Bitfinex chief technology officer and incoming Tether CEO, said the “exciting” initiative marks the beginning of a new era in capital raising.

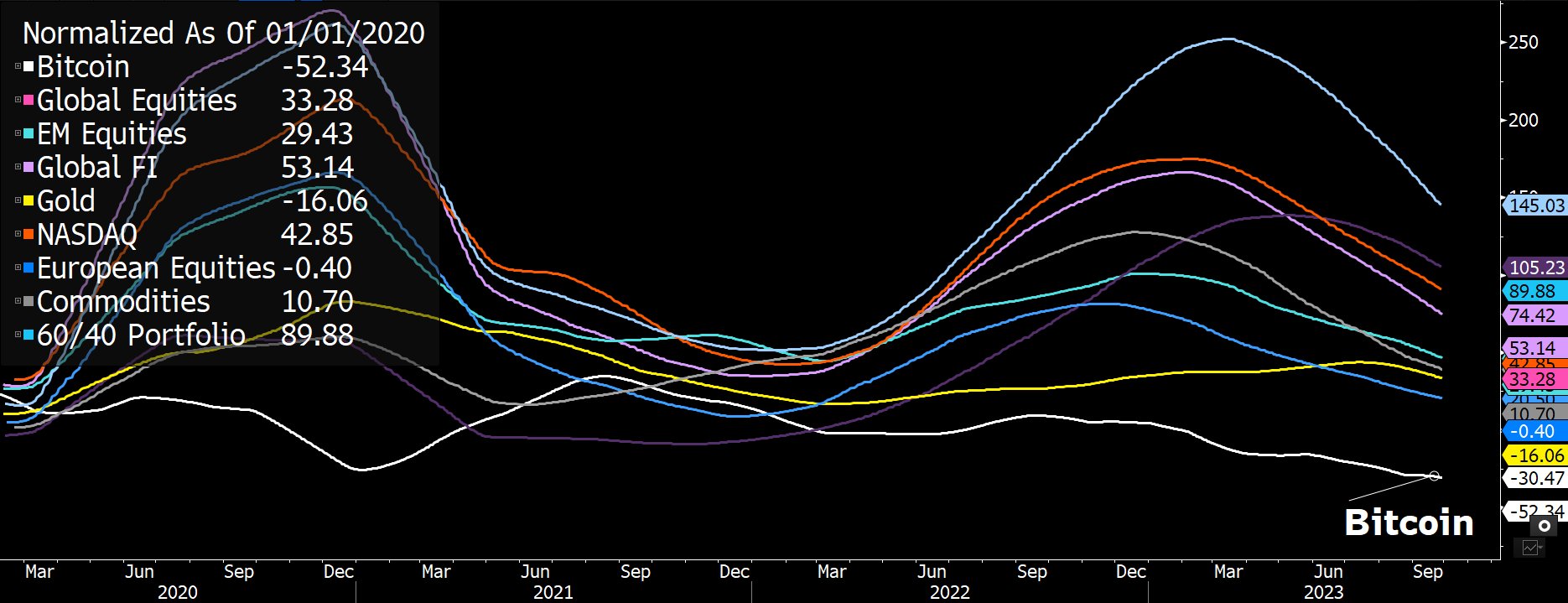

In a comprehensive evaluation of global market dynamics, Bloomberg Intelligence analyst and Chartered Market Technician (CMT) Jamie Coutts has opined on the shifting sands of financial asset volatility. With bonds potentially falling out of favor and Bitcoin cementing its place as a debasement hedge, traditional portfolio models may be on the verge of a renaissance.

Coutts tweeted, “It looks like we are about to see a substantial uptick in volatility across all markets, given where yields, USD, & global M2 are heading. Despite what lies ahead, there has been a big shift in the volatility profiles of global assets vs. Bitcoin over the past years.”

A comparative analysis by Coutts highlighted that since 2020, the volatility profiles of Bitcoin and Gold have declined, while most other assets have seen an increase in volatility.

His breakdown indicates that the traditional 60/40 portfolio volatility is up by 90%, NASDAQ’s volatility has surged by 53%, and global equity volatility rose by 33%; meanwhile, only Bitcoin’s volatility decreased by 52% as well as Gold’s volatility, which went down by 6%

Coutts further elaborated that following the “hyper-volatile” phase of Bitcoin during 2011-14, the cryptocurrency’s volatility has been on a downward trajectory. From a peak above 120 in early 2018, this metric currently stands at 26.39.

However, Coutts maintains skepticism over Bitcoin’s short-term prospects given the deteriorating macro environment: “Given that BTC volatility is near the bottom of the range plus a deteriorating macro environment: US dollar (DXY) is up, 10Y Treasury Yield is up, Global M2 money supply is up. It’s difficult to see how BTC (& all risk assets) can hold up with this setup.”

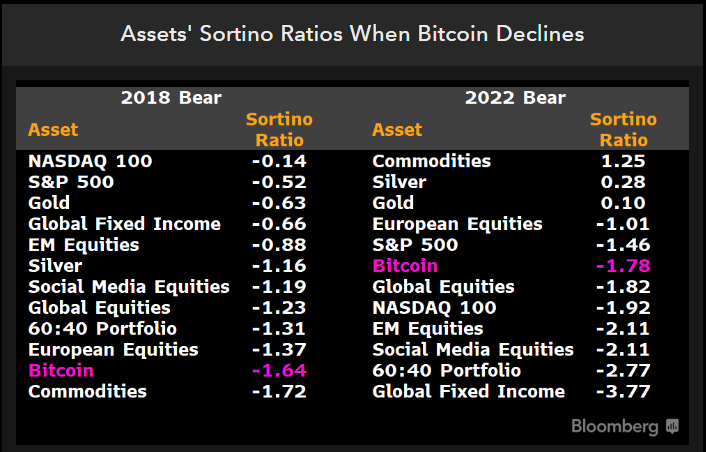

On the bright side, from an asset allocation perspective, Coutts considers the real question to be whether “Bitcoin can add value as a risk diversifier & improve risk-adjusted returns.” Comparing the risk-adjusted returns using the Sortino ratio during the last bear market, Bitcoin’s performance is not the best.

In the 2022 bear market, Bitcoin’s Sortino ratio is -1.78, positioning BTC above global equities, the NASDAQ 100, and the traditional 60:40 portfolio. However, it trails the S&P 500 (-1.46), European Equities (-1.01), Gold (+0.1), Silver (+0.28), and commodities (+1.25).

Elaborating on the cyclical behavior of Bitcoin, Coutts added, “The problem with BTC is the relatively short history makes inferences difficult and 1 year periods are certainly not significant. The best we can go on is multiple cycles. It’s clear that holding over the full cycle has been a winning strategy.”

Evaluating the Sortino ratio over the past three Bitcoin cycles (2013-2022), Coutts found Bitcoin to lead with a score of 2.46, outperforming the NASDAQ 100 (+1.37), S&P 500 (+1.25), and global equities (+1.05).

In this scenario, Debasement concerns further enhance Bitcoin’s proposition. Coutts emphasized this saying, “And if allocators want to outpace monetary debasement, over most timeframes, bonds are not the place to be.” He identified Bitcoin as the foremost choice for portfolio reallocation against monetary debasement.

Citing the vast difference between asset returns concerning money supply growth (M2) over the past 10 years, he highlighted Bitcoin’s dominance with a staggering ratio of +8,598, followed by NASDAQ (+109), S&P 500 (+25) and global equities (-7.5).

In a concluding statement, Coutts postulated, “In the years ahead it’s conceivable that allocators begin to shift towards better debasement hedges. BTC is an obvious choice.” Moreover, he suggests that Bitcoin could supplant bonds by securing at least 1% of the traditional 60/40 portfolio.

At press time, BTC traded at $26,433.

Todd Groth of CoinDesk Indices explores the relationship between interest rates and bitcoin.

Incorporating AI and DLT into business models may require “substantial investment” at first – but could help lower expenses and improve market liquidity over time, a new report said.

The monetary authority in Hong Kong released a report on its study Project Evergreen which looked at the highs and lows of recent bond tokenization activity.

Two investment moguls are betting on different directions for inflation and Treasury yields, with potentially negative impacts on Bitcoin.

The rise in real yields is more of a headache to blue chip stocks than to markets like technology or crypto and will not disrupt the medium-term growth story, one observer said.

The future of debt instruments is being built today, Arca’s Anthony Bufinsky writes.

The platform makes the first use case of a so-called “Proof of Climate” blockchain protocol.

The platform will use Proof of Climate awaReness as a validating protocol to encourage users to minimize their environmental footprint.

Treasury curve suggests the widely-anticipated U.S. economic recession is near. Historically, the signal has brought pain to risk assets.

Swiss commodities trading firm Muff Trading AG issued corporate bonds using Obligate’s decentralized finance platform, which is set to open to the public on 27 March.

The emergency proposal increases MakerDAO’s holdings of United States bonds by 150%, aiming to diversify the Dai stablecoin’s collateral exposure.