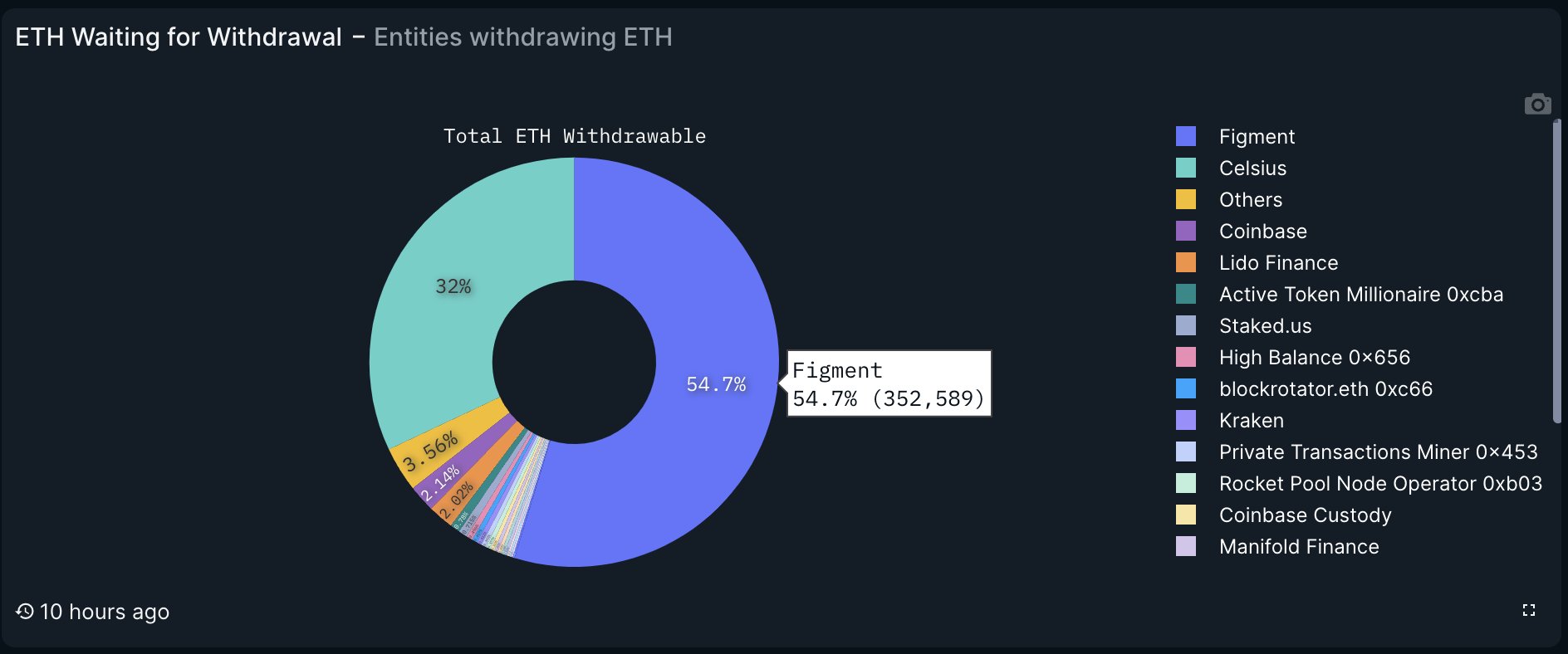

According to a Bloomberg report, Celsius Network, the crypto platform that filed for bankruptcy in July 2022, demands that major customers who collectively withdrew over $2 billion before the bankruptcy return those funds to avoid potential litigation.

An oversight committee formed during Celsius’s Chapter 11 case has begun contacting customers who withdrew more than $100,000 during the period leading up to the company’s bankruptcy filing. This recovery effort aims to repay creditors who did not withdraw funds from Celsius.

Settlement Offered To Celsius Users

Per the report, the oversight committee’s recovery process will impact around 2% of Celsius users who, in total, withdrew approximately 40% of the platform’s assets within the 90 days preceding the Chapter 11 filing.

Celsius reported $6 billion in assets, 1.7 million registered users, and 300,000 active users with account balances exceeding $100 at the time of bankruptcy.

Notably, the oversight committee has offered customers who may face clawback suits a settlement option, providing them with a “favorable rate” if they choose to settle.

Customers who opt for settlement would have their potential liabilities determined based on the value of their assets at the time of their 2022 withdrawals. This means that settling customers would retain any appreciation in the value of their digital assets resulting from the surge in crypto prices over the past year.

Legal Consequences If Settlement Offer Is Declined

According to Bloomberg, customers who decline to settle may be subject to significantly more liability through potential litigation. The committee’s letter warns customers about the potential consequences of not accepting the settlement offer.

In November, a bankruptcy judge approved Celsius’ plan to distribute billions of dollars in assets and transform into a creditor-owned Bitcoin mining firm. According to a court filing by the company’s lawyers, Celsius has already distributed around $2 billion in assets.

Overall, Celsius Network’s oversight committee is pursuing the recovery of over $2 billion in withdrawals made by major customers shortly before the company filed for bankruptcy. By offering settlement options based on the value of assets at the time of withdrawal, Celsius aims to alleviate potential litigation and expedite the repayment of creditors.

As the process unfolds, impacted customers decide to settle potential liabilities or face potential litigation with potentially higher consequences.

Currently, the network’s native token, CEL, is trading at $0.1862, reflecting a significant year-to-date decline of over 49%.

In shorter time frames, the token has experienced a 12% decline in the last 24 hours, a 32% decline in the last week, and a 27% decline in the last fourteen days, highlighting the limited interest and lack of confidence among investors in the CEL token.

Featured image from Shutterstock, chart from TradingView.com